I'm interested in something somewhat different. So from the Keynesian perspective statements like "an income based measure of output and an expenditure based measure of output should be equal" needs a little more elaboration, because the Keynesian point is precisely that it's the process that makes these two equal that is so essential to understanding the business cycle.

So what is a business cycle? The most fundamental description is that it's when expenditure is "trying to be lower" than income, and income is adjusting dynamically. There are a couple different processes to look at when we talk about the dynamic adjustment: (1.) consumption behavior and the multiplier, (2.) money demand, interest rates and investment demand, etc. But that's the story in a nutshell.

UPDATE: I read the graph wrong - read the comments below for details and for some thoughts on what is going on. Bob Murphy talks about it here too. Any other ideas?

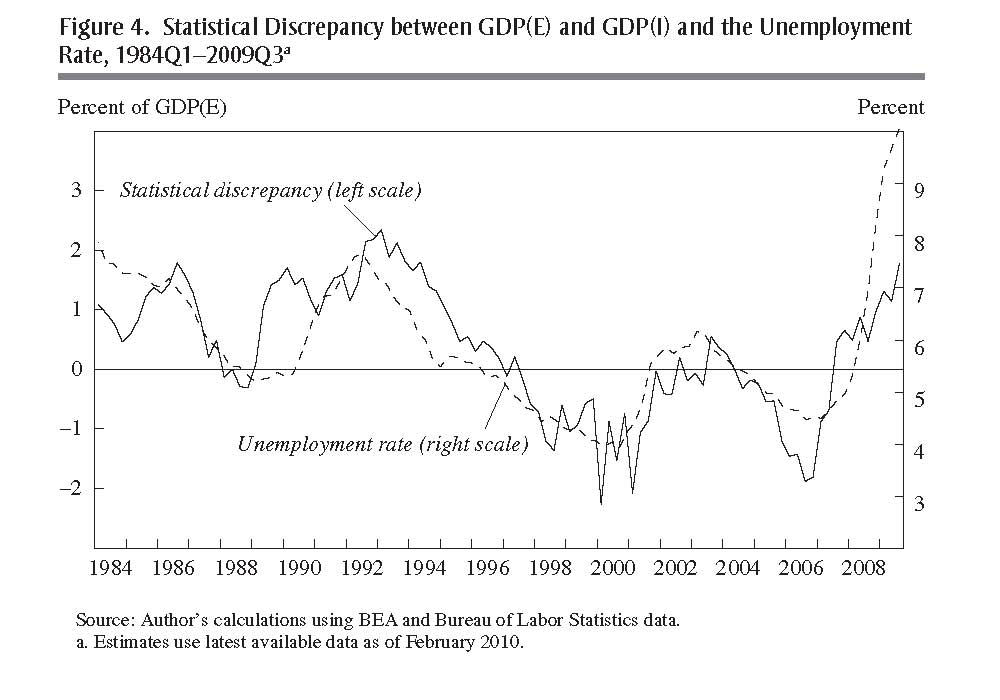

Which brings us to figure four in the Nailewaik paper (page 88). Now that is a fantastic graphic:

That's a lot of correlation right there.

ReplyDeleteAnd it's correlation of a statistical discrepancy of all things - a discrepancy which they claim ought not to exist (which seemed a little weird to me from the beginning). Now, of course we ought to be careful when thinking about the causal ordering of correlations, but the point is this - something that you might have expected to be noise clearly isn't just noise, and that means something. I've only gotten a chance to read portions of the paper, but so far they don't seem to discuss this issue at all.

ReplyDeleteWait a minute Daniel--you're saying the authors just decided to put in that chart, even though they don't think it might have to do with what you're talking about in this post?

ReplyDeleteAlso, is their discrepancy measuring GDP(E) - GDP(I), as the title of the graph suggests? If so, isn't that the opposite of what you were postulating?

ReplyDelete(I'm not knocking your blog post; I think it makes a lot of sense. I'm just looking at the way they titled their graph.)

Yeah, I think they titled their graph correctly, Daniel. Because their big headline result is that in terms of income, GDP started tanking in late 2006, right? So if GDP(I) started dropping relative to GDP(E) in late 2006, then the rising discrepancy starting around that point means that the graph is definitely charting GDP(E) - GDP(I).

ReplyDeleteHence, either you got Keynesian theory backwards, or this chart refutes it. I will let you decide. :)

Bob, E - I went negative for a couple of years before the recession started. I think that's what Keynesians would predict.

ReplyDeleteDaniel: Three Words: "Unplanned Inventory Accumulation" - This is a component of expenditure in the national accounts, no? In theory, it should equal Income less Conventionally defined expenditure, so that NIA Expenditure always equals Income.

ReplyDeleteBob - I went back and read that - you're exactly right!

ReplyDeleteSo what would cause that? Kevin's point about inventory accumulation would work against that too, would it not? So I'm not sure that's what we're seeing (it would make sense if my backwards reading of it was right!).

Perhaps this is a matter of life cycle consumption - you're purchasing a constant share of your present value of life-time income, so when national income drops more of that is purchased with credit or out of savings? I suppose that would make sense.

Yes - that's not nearly as interesting. That's not a macro story at all - that's just some micro common sense :)

Gene's point is interesting too - the negative expenditure shock caused the unemployment, and then the recession caused the spending out of savings/on credit.

ReplyDeleteAny other thoughts on this?

Thanks for catching that Bob.

Damn! It just ate my comment!

ReplyDeleteWhat that chart shows is an error in the data. Or, more precisely, the difference between those two series is the difference between 2 errors in the data. By itself, it cannot support or refute any theory.

What we need, and what I have yet to see, is some person who works at the coal face of statistics who understands the nitty gritty of where that data comes from who can explain to us what that data error is likely to mean.

So I don't understand why there's this presumption that one measure is better than another - and perhaps you can shed light on this, Nick.

ReplyDeleteYes all income is expenditure, and I could imagine one is an "error" insofar as perhaps (because of credit), expenditure could lead income measures. I get that. But I don't see why Kling and Wolfers and the author are talking about why GDP(I) is better because it is more sensitive to business cycle indicators. I imagine nominal GDP is more sensitive to business cycle indicators than real GDP too. That doesn't mean it's "better" than real GDP at being a measure of output.

It seems to me we shouldn't be talking about GDP(I) or GDP(E) being better than each other - they're just measuring different things (both imperfectly).

Dan: "It seems to me we shouldn't be talking about GDP(I) or GDP(E) being better than each other - they're just measuring different things (both imperfectly)."

ReplyDeleteNo, they are both measuring the *same* thing, both imperfectly. GDP(I) and GDP(E) ought to be exactly the same, if we collected our data perfectly. RGDP and NGDP ought (almost always) be different, because they are measuring different things.

Suppose you had two thermometers outside your house. And they both give different readings, and you know that both are crappy cheap thermometers. But you notice that thermometer A has a better correlation with snow than thermometer B. You *might* infer from that that A was more accurate than B. But that's just a hunch. An alternative inference is that A is measuring a mixture of temperature and humidity, which makes it a crappy thermometer, (but still an interesting measure of something).

Maybe the answer is income tax evasion. People will tend to declare their expenses faithfully and conceal part of their income especially during recessions.

ReplyDeleteIn any case, as Nick Rowe pointed out, this proves nothing wrt keynesianism, it only shows something about how the data is gathered.