What I want to demonstrate (in response to this post) is my own answer to why Keynes wrote in the General Theory "I was brought up to believe that the attitude of the Medieval Church to the rate of interest was inherently absurd... but I now read these discussions as an honest intellectual effort to keep separate what the classical theory has inextricably confused together, namely, the rate of interest and the marginal efficiency of capital".

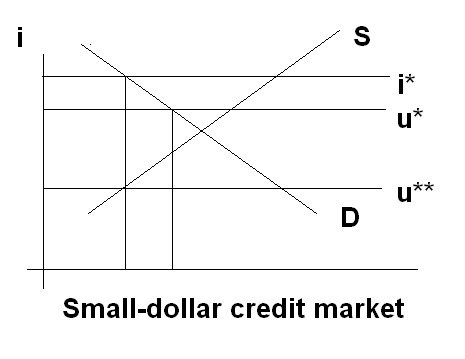

So first you have the market for small-dollar loans (payday loans, pawnshop loans - the credit market that users of these products are in). Economics 101 says the interest rate in this particular loanable funds market is going to be at the equilibrium of supply and demand - pushing the interest rate too low will limit supply and hurt the poor. However, the story changes if liquidity preference drives the interest rate (i*) too high. Now we have a shortage of credit to the predominantly low income families that use these sorts of loans.

It's not entirely clear, in this circumstance, how we should view usury laws. There is wide latitude for being indifferent to laws that restrict interest rates. If a usury law sets permissable interest rates at u*, we see an increase in the number of loans made and a reduction in the cost: a net increase in social welfare. In fact any rate between i* and u** will increase social welfare. Any rate below u** (or an outright prohibition) will reduce social welfare.

It's not entirely clear, in this circumstance, how we should view usury laws. There is wide latitude for being indifferent to laws that restrict interest rates. If a usury law sets permissable interest rates at u*, we see an increase in the number of loans made and a reduction in the cost: a net increase in social welfare. In fact any rate between i* and u** will increase social welfare. Any rate below u** (or an outright prohibition) will reduce social welfare. Does this sound implausible to people? Take a look at Table 4, on page 29 of the recent report on these small-dollar credit products that I recently co-authored. I was surprised to see this result myself, and although it's hard to know what to make of it it's indicative. We predict usage of these products, controlling for the amount of the price cap in force in the state, and we include a dummy variable (i.e. - a variable that equals zero or one) to indicate whether there was no cap. This allows the usage rate for people in states with no usury law to vary from the trend line estimated for states with a usury law (see the illustration below). What we found was that for payday loans and especially for auto title loans, usage rates declined when there were no usury restrictions at all! That's not supposed to happen in the Econ 101 model! It makes sense in this Keynesian model (and there are a few other credit rationing models - notably Stiglitz and Weiss (1981) - which also predict this behavior).

Does this sound implausible to people? Take a look at Table 4, on page 29 of the recent report on these small-dollar credit products that I recently co-authored. I was surprised to see this result myself, and although it's hard to know what to make of it it's indicative. We predict usage of these products, controlling for the amount of the price cap in force in the state, and we include a dummy variable (i.e. - a variable that equals zero or one) to indicate whether there was no cap. This allows the usage rate for people in states with no usury law to vary from the trend line estimated for states with a usury law (see the illustration below). What we found was that for payday loans and especially for auto title loans, usage rates declined when there were no usury restrictions at all! That's not supposed to happen in the Econ 101 model! It makes sense in this Keynesian model (and there are a few other credit rationing models - notably Stiglitz and Weiss (1981) - which also predict this behavior).

Now - it could be a few other things. We could be dealing with some endogeneity here. States without big small-dollar loan problems or markets might be less likely to implement laws. This could be an issue with the estimate, but (1.) we controlled for a lot of individual and state level variables that you traditionally think of as being associated with these issues, and (2.) if we did have some endogeneity on our hand, you would expect the coefficient on the price cap variable to be negative as well - we don't see that.

Several of our products didn't even have interest rate caps to speak of, and these are just two tenuous results - but it's interesting enough to see that that I think it's worth investigating further (and I hope to some day). There's more that can be done with the data we used, and there are some other data out there that could corroborate. The point is, at this point the story I told above is not a crazy story.

Where does that put us with usury laws? Well - outright bans of usury are still not a good idea, whether you're coming from this Keynesian model, the economics 101 model, or the Stiglitz and Weiss (1981) credit rationing model. But it says we shouldn't be too knee-jerk about some restrictions on interest rates, and it suggests that the old usury opponents in the early Church and even back to ancient times might not have been entirely crazy. Like the mercantilists who were grappling with a proto-monetary disequilibrium theory, the usury theorists were thinking more deeply about interest rates and the loanable funds market than a lot of people who just parrot the textbook model do. It doesn't make them right - but they were may have been "wrong for the right reasons".

And I should note - there's a whole other group of people that says my demand and supply curves are meaningless because people don't know what they're getting into and lenders are predatory.

ReplyDeleteLet's be honest - predatory lending does go on. People aren't well informed about these things. These are real issues that oughta be addressed with fraud enforcement, financial education, etc. The economic analysis should not be ground to a halt because of these issues, but we also shouldn't forget about them.

You know what he says about the medieval church...

ReplyDeleteMurray Rothbard said that some of Keynesian economics had roots in medieval feudal thought.

Did you ever find it interesting that Keynes was both a progressive and retrogressive economist? That, on one hand, he want to discard and move further ahead from the orthodoxy of the day that he loathed and, on the other hand, he wanted to reach into older tradition to move away from fashionable present day ideas?

Another way of putting that, Prateek, is that it was nineteenth century economics that was retrogressive and Keynes put us back on a progressive trajectory!

ReplyDelete