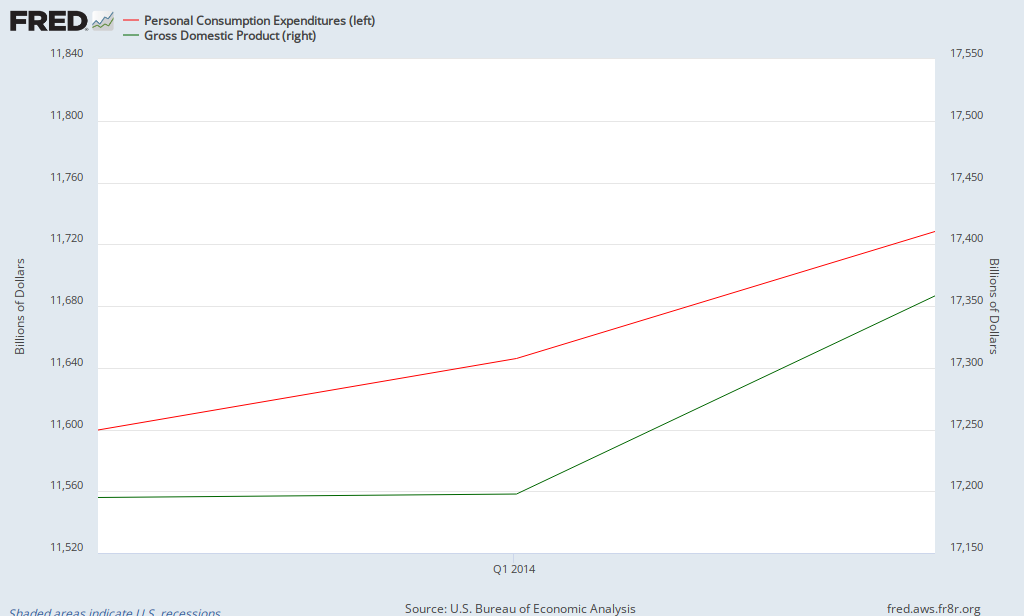

"Real personal consumption expenditures peaked in late 2007 before the recession and by late 2010 had already recovered to that peak. Consumption today is well ahead of that peak and up substantially from its weakest point in mid-2009. The economy is not suffering from lack of consumer spending, putting a substantial dent in Rawlins’s case for more government spending on consumer stimulus."I have a lot of trouble with claims like this because of the graph below. GDP is on the the right axis, while personal consumption expenditures are on the left axis. If your only evidence is that we've passed the 2007 peak, then we've got no GDP problem either! In fact, while both have exceeded their previous peak both are still well off trend, which is why employment has not reached its previous peak.

Now I can't see how anyone can look at that graph above and say we don't have a consumption problem, but in the title of this post I did say "yes and no". Why? Because Steve is right when he says this:

"The problem instead is private investment spending. One of the first things economists teach about business cycles is that the most variable part of spending is not consumption but the investment that firms make in capital. Private investment spending has only recovered about half of its losses from the recession. Firms are simply not willing to invest in the equipment and research and development to make new products and create new jobs. That is the problem to be solved."He is right of course. I taught that to my macro students. I was taught that by every macro professor I had. And the fact is no business cycle theory that fails to say this has ever survived in macro because it's so obviously untrue. Now that doesn't mean we are silent on consumption. Consumption shocks are possible and there's a mountain of research on consumption behavior. But it's not the decisive factor in the business cycle.

I don't think this justifies the first paragraph, though. We do have a consumption problem. Some of it may be exogenous to the recession itself. Stiglitz has been making the point recently that inequality depresses consumption levels. That's certainly sensible. But to explain the very real problem with consumption in the graph above, you really have to recognize that the consumption problem is (1.) real, and (2.) a consequence of the recession. People consume less because they have less money than they used to, and they have less money than they used to because of investment problems. Low consumer demand does make things worse - it does pin us down - in the sense that declines in investment and government spending (relative to trend, remember!) are multiplied by the behavior of consumers.

So what about the solutions?

Increasing consumption exogenously will help as much as increasing investment exogenously will. And for humanitarian reasons alone we ought to have some of our recovery effort come through consumption-oriented spending. But since consumption is not the heart of the problem, I don't think that should be the end of the story. The real problem we need to solve is the investment problem.

You're arguing from a tautology because of how GDP is described and measured.

ReplyDeleteDaniel, it appears to me that you so deeply misunderstand what is the means and what is the ends that it's become pointless to debate. More or less everything I would want to say about this post was put into my Forbes piece.

You can NEVER have a "consumption problem" in and of itself. ALL "consumption problems" are the result of either ineffective production or, on the demand side, monetary disequilibrium leading to coordination failure.

The demand for commodities is NOT the demand for labor.

Put up more graphs. Show total workforce size. Show participation of working-age males. And compare those to "consumption spending" vs. "investment spending".

You're analysis is simply wrong. Deeply wrong.

Consumption doesn't create new jobs and doesn't increase output. Period. But if you want more data or rebuttal than that, it's all in this link:

http://www.forbes.com/sites/beltway/2013/01/30/think-consumption-is-the-engine-of-our-economy-think-again/

"Stiglitz has been making the point recently that inequality depresses consumption levels. That's certainly sensible."

ReplyDeleteHow is this remotely "sensible"? The actual data doesn't support that in the least. Consumption has been rising as a share of GDP throughout the period in which Stiglitz asserts that inequality has been rising.

The only way for this fact-free assertion to be "sensible" is if Stiglitz makes the Malthusian mistake of conflating savings with hoarding. Since the data doesn't support the assertion and savings isn't hoarding, good old Adam Smith economics holds (all that is saved is consumed by other people) and Stiglitz's view is not sensible at all. It is fallacy.

I'm not clear on why Stiglitz implies that the consumption share can't be rising, John. There are underlying reasons why the investment share of GDP in the U.S. might be undergoing a secular decline while it might be on the rise in a place like China. That doesn't mean Stiglitz is wrong at all.

DeleteIt's true that the consumption share of GDP can rise while at the same time there's a force depressing consumption levels. Suppose inequality is causing consumers to spend less, and meanwhile something else more powerful is causing investors to invest less. But, it needs proving that this is what's happening. Hans-Hoppe thinks that Monarchy is a better form of government to Democracy. When someone asks "But what about all the progress the world have made under Democracy?" He says "It would have made even more progress under Monarchy". You have given about as much evidence as he generally does.

DeleteI agree with John Papola that inequality can't have an effect in the long-run. Citing long-run fluctuations in equality as exacerbating recessions is rubbish. Just for variety I'll give a slightly different explanation, though I think John's is fine....

Let's suppose that at year 0 inequality increases substantially. The poor consume a larger percentage of their income than the rich. The rich save more, and those savings are invested. So, when inequality increases there's a shift to lower consumption spending. If we're at year 30 and there's a recession it makes no sense to blame that on the increase in inequality that occurred at year 0. Pretty much the same thing is true if the change is spread out over time, if inequality increases a little every year. It's not unreasonable to blame a decrease in consumption spending in year 30 on the inequality increase that occurred in the few years before, but it is unreasonable to blame what happened decades ago. And if the small change that occurs over a few years had no noticeable effect in the past then why should we suspect it in the present?

What Stiglitz is seems to be really saying is if a large amount of wealth were redistributed now then demand for consumption goods would increase. That's quite true but, and I don't think anyone would dispute it. But, then the question arises: what's the cost of doing that?

Daniel, I think it's time to post about a bunch of stuff the you've read on the internet again. That'll make sure that the stupid stuff you said here and in the previous post comparing immigration and the minimum wage will drop off the bottom of the blog into "Older Posts". ;)

Right - but I'm not saying that inequality caused the recession through its impact on consumption, and although I haven't read his book I don't think Stiglitz says that (if he goes that far, we disagree). I'm saying the secular trend in inequality depressed consumption levels.

DeleteIt's very easy to explain why as a long run trend for other reasons consumption shares would increase - we're a mature industrial economy. It's just a basic long-run convergence point.

I make a rule of not saying stupid things on the blog :)

Often what is imputed to me can be pretty stupid, it's true!

What was wrong with the minimum wage point? Surely you can appreciate that people almost exclusively focus on the partial equilibrium points of that, can't you? We should expect a big negative effect if that's our only window. The fact that we see more mixed results (mostly negative to be sure, but not entirely, and only modestly negative) suggests that's probably too simplified of a take on things.

DeleteIf all he's saying is that the secular trend in inequality depresses consumption levels then he's right. But, the inference seems to be that it makes the economy worse in the long-term. That's wrong, because in the long-term savings drive investments, even if flights-to-quality occur in the short-term. So, the extra savings of the rich allow for greater capital investment, which is to everyone's benefit in the long-run. Of course inequality may damage growth through other factors, but depressing consumption in favour of investments over the long-term is not one of them.

DeleteThe minimum wage point is a mess, for the reasons I mentioned in that thread.

1) You don't take into account the consumption demand that would occur from those priced out of jobs by the minimum wage.

2) You assume that employers earn a large profit on minimum wage jobs, so some of that can be taken without increasing unemployment. But, that can't *always* be the case, because firms will expand until taking on more people is unprofitable.

3) You can't take the propensity to spend on GDP goods of businesses and consumers to be fixed. In time business will expand it's spending.

4) You also have the problem that less hours worked may mean less capital accumulation and lower growth.

Current, I'm not saying you can just point to general equilibrium and say the minimum wage is fine. I'm saying people rarely talk about that.

DeleteIn other words, your 1), 3), and 4) are all exactly what I'm saying we should be thinking more about instead of always pulling out the partial equilibrium!!!

I offered one general equilibrium point that would be a good explanation for why the data is mixed and modest. I'm not claiming I've tracked down all the relevant general equilibrium points in a single blog post!

I also don't think I've done 2) at all.

"I'm not saying you can just point to general equilibrium and say the minimum wage is fine. I'm saying people rarely talk about that."

DeleteFair enough, but you're only pointing out the general equilibrium effects that help the case for it, not those that don't.

In 2) I was criticizing one of the justifications normally given for minimum wages. I agree you didn't give that reason in your post.

If capital goods are falling in price, the economy can grow even as investment falls.

ReplyDeleteYep, this too.

DeleteDon't pay too much attention to John.

"Consumption doesn't create new jobs and doesn't increase output. Period. But if you want more data or rebuttal than that, it's all in this link:"

ReplyDeleteWhen a company invest and buy say new machines it actually operate as a consumer for an another company. Investment is a 'bet' on futur profit itself based on futur sales that is : consumption.

Profit is the spending of another. If consumption play no role at all, then wage set to zero would have no effect on economy, a point that seem dubious even for a non economist like me.