*****

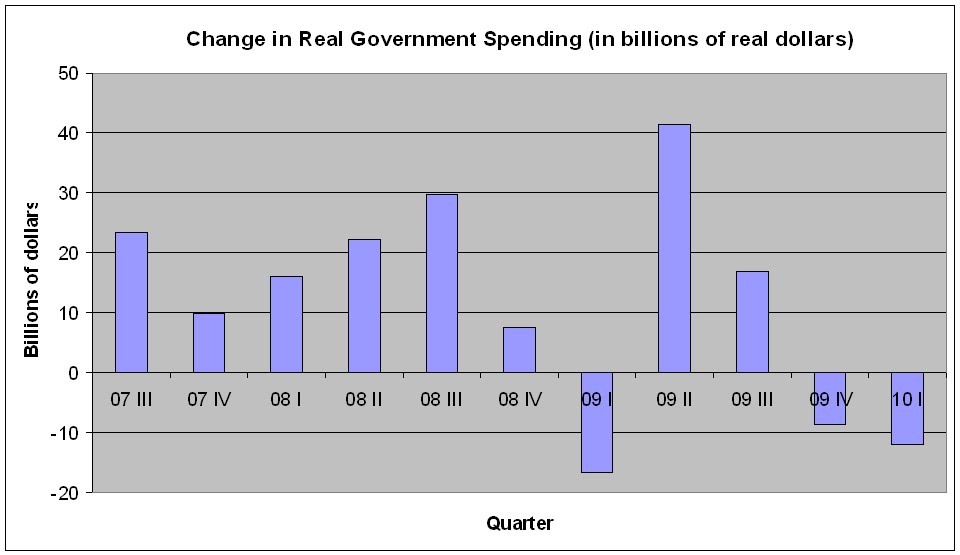

"The American economy faces a major threat to economic recovery that most of the public probably isn’t aware of: government has been slashing spending for the last nine months. This Friday it became official when the Commerce Department released its quarterly economic statistics. In the second quarter of 2010, total government spending fell by [X] percent. In the first quarter of 2010, it had been reduced by 1.9 percent while in the fourth quarter of 2009 it dropped by 1.3 percent.

Recently, economists have been debating the merits of precisely this kind of “austerity.” Some have argued that reducing public spending can spur economic growth. Others are convinced that it is a sure way to kill the recovery. This discussion has generally revolved around Europe, which is increasingly pursuing austerity measures, and whether Europe offers a model or a cautionary tale for the United States. What this debate often leaves out is that belt-tightening by the government has already come to our shores, and it has been with us for the better part of a year now.

This seems to contradict what everyone knows: that the Obama administration has been running record-breaking deficits. Politicians and cable news commentators bombard us with concerns about our profligacy over the radio during our commute to work every morning and on television every night. How can it possibly be true that government has been slashing spending for the past nine months?

What the public often forgets is that the United States is a federal system with state and local governments as well as a federal government. We don’t “forget” about federalism in the sense that we don’t realize these other levels of government exist; they are an important part of our lives. But we do forget their relevance to problems of national significance, such as the current recession. This is a serious oversight, because together state and local government budgets are about one and a half times the size of the federal budget. That means that amidst all the discussion of the role of government in the economy during a downturn, many of us are completely forgetting about a significant portion of the government spending that goes on. Unfortunately, the economy and the job market don’t have the luxury of forgetting this. The economy can’t tell the difference between a dollar appropriated by the federal government and one appropriated by a state or local government.

Government spending has been shrinking for the last nine months because the federal government has been almost entirely preoccupied with filling in the hole that state and local governments have been digging, and the states have been digging that hole faster than the federal government has been filling it since the third quarter of last year. This results in a net reduction of government spending in the United States. If you think that government spending during a recession is harmful, you may be comforted by this news. However, those inclined to celebrate this reduction in government spending should consider the fact that the economic outlook began to darken again precisely when total government spending (federal spending, plus state and local spending) started to shrink.

Austerity is pursued in state and local governments for many reasons. Municipal bond markets aren’t always as accommodating as the market for federal debt. Some of these entities are constrained by balanced budget requirements in their constitutions, or statutory limitations on running deficits. Local governments that rely on property taxes have been hit hard by the housing crash. In addition to all these real constraints, though, a lot of state and local leaders simply believe that tight-fistedness is a virtue during a recession. Many governors, mayors, and county boards don’t seem to have received the memo from much of standard economic theory that responsible governments are supposed to lean against the economic winds. They should take a step back when the economy is heating up and government spending risks crowding out private activities and jump in to buy and use idle resources when the private sector is too fearful of what the future holds.

While some states, such as California, have a legitimately difficult time convincing creditors to lend to them, others, like my home state of Virginia, have no such excuse. Virginia has an excellent credit rating, but our governor and our state legislature apparently feel an abiding need to run a budget surplus during the worst downturn since the Great Depression. This decision in Richmond has the same impact on the economy as the recent decision of many big businesses to sit on profits instead of using that income to hire and invest. The Virginia state government is essentially telling us that it makes more sense to sit on our tax dollars right now than it does to use them to put unemployed Virginians and unused equipment to productive work. Yet for this, Governor McDonnell gets celebrated by voters and the press.

The growth of the federal government in the decades since the last downturn of this magnitude in the 1930s leads many Americans to forget about the significance of our federal system of local, state, and national governments. The public debate over economic policy is distorted by the fact that we’re not even talking about the majority of government spending that occurs outside of the federal government. Those of us who acknowledge the importance of stimulus get complacent because we aren’t aware that government spending is actually being reduced right now, not increased. Those who argue against stimulus are galvanized by false claims that total government spending is soaring.

State governments have always played a fundamental role in the history of our republic, and they are just as essential today as they have been in the past. We can no longer afford to write them out of the story of the government response to the recession."

*****

The argument itself still stands, of course. The logic is still good, and we still overestimate how much fiscal stimulus we're doing because we forget about the states. The positive numbers for quarter-to-quarter change this quarter are also probably related to several previous quarters of negative growth in government spending (i.e. we're still down from where we should be but they can't fall forever so you're going to get periods of positive growth). But it's harder to make that case convincingly when one of the three quarters you're looking at runs against your thesis.

So how do we interpret these recent GDP numbers?

1. It's good news public spending is not shrinking again. Private spending probably would have looked better if we didn't have six months of austerity at the end of 2009 and the beginning of 2010.

2. Fiscal policy has a lag, just like monetary policy. Shortly after spending initially stalled out we saw a weakening (also due to the fiscal crisis). Then public spending picked up dramatically with the stimulus package, after a quarter or two GDP did too. Then after an early spring of weak stimulus, we're seeing a continued weakening in GDP. In three to six months we may see another upward trend (hold me to it - we can check the data) as a result of this increase in fiscal stimulus, but a lot of that depends on whether it is sustained through the third quarter and what else happens.

3. This all is just going to contribute to confusion over what is exactly going on, which is unfortunate. We're still doing tepid, on again-off again stimulus which isn't good for the economy or for clear analysis. Informally eye-balling it, we're seeing a something like a delayed wave pattern (I demonstrate it here) with output lagging a quarter or two behind public spending. We shall see, though.